The financial world is loaded with jargon. You’re dealing with company ownership with both an Employee Stock Ownership Plan (ESOP) or an Employee Stock Purchase Plan (ESPP). These plans were created with the intent to help employees create and build wealth, but ESOPs specifically can also provide benefits for business owners. We’ll break down the differences.

How they’re structured

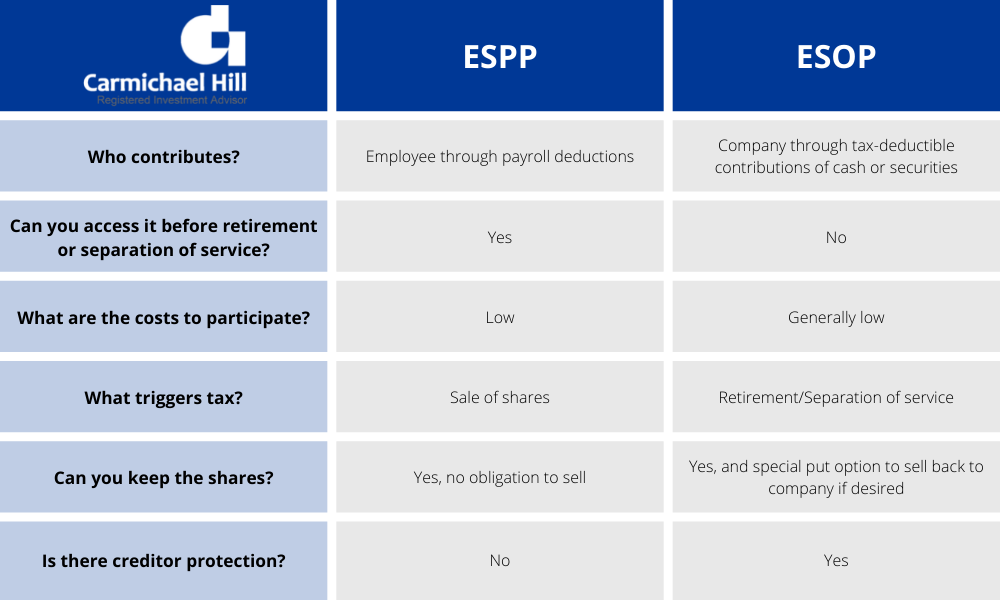

ESOP

ESOPs are qualified defined contribution plans established by the Internal Revenue Code and governed by the Department of Labor. These are ERISA plans, which means they get the same special treatment and protection under law as a 401k. A company will establish one of these by setting up a trust account and depositing company shares (or depositing cash that is then used to buy company shares). These contributions are deductible to the company up to certain limits.

These shares are then apportioned out to individual employee accounts. There are different methods and formulas to determine who gets what, but the company that decides this. Contributions are made by the company on an annual basis. Most ESOPs use a 3-6 year vesting schedule just like a 401k.

ESPP

An ESPP is a different animal. This is not a qualified plan and employers do not contribute. This is simply an opportunity to purchase company stock at a discount, usually somewhere between 5-15% off the fair market value. The purchases are made with after-tax payroll deductions at pre-set dates. Unlike an ESOP, you aren’t automatically enrolled in this plan. Participation is entirely optional.

These plans have an offering period, which is the period in which your contributions accumulate before they are used to buy stock. The purchase period is the shorter window of time during which you can use that pool of money to buy shares. The purchase date is when you actually buy the shares, the purchase price is what you pay, and the sale date is when you cash out and sell your shares.

Not all plans are uniform. Some have a “lookback” feature, which is an absolute gift if your plan has it. This compares the stock price at the beginning of the offering period to the purchase date and applies the discount to whichever stock price was lower.

For example, say the share price was $100 on the offering date and rose to $150 by the time of purchase. The discount is 15%. A lookback feature would apply that discount to the $100 price, thereby taking it to just $85!

Taxes

Taxes are straightforward on an ESOP. The company buys back your shares when you separate from service and sends you a check. The liquidation triggers ordinary income taxes, but you can defer these by rolling the proceeds into another pre-tax account like a 401k or an IRA. You only get dinged on whatever isn’t rolled over.

There is one special caveat to the ESOP: Net Unrealized Appreciation (NUA). This special tax treatment allows ESOP participants to distribute stock to a taxable brokerage account while paying ordinary income tax on just the basis and long-term capital gains on the appreciation. This may not seem like much, but the top ordinary income tax rate in 2022 is 37%. The top capital gains rate is just 20%. NUA treatment could allow for significant tax savings if there is significant appreciation in the shares you own from the ESOP!

ESPPs are more complicated. There are qualified ESPPs and non-qualified ESPPs, and within the qualified ESPPs there are qualifying and non-qualifying dispositions! Your final tax bill will differ depending on what kind of ESPP you have and the type of disposition that takes place. Generally, you can get preferential tax treatment if you hold onto the shares you acquire for at least one year from the purchase date and two years from the offering date.

Liquidation

You can take shares acquired through an ESPP with you when you leave. The same is true of ESOPs, but it works slightly differently with a closely held business. Section 409(h) of the Internal Revenue Code says that employees that receive stock from a closely held business have the right to require the business to repurchase their ESOP shares.

This effectively gives employees a put option to sell shares back to the company if they want to liquidate and walk away. The requirement is there to protect employees who may not be able to sell the shares otherwise.

Costs

Both plans are generally exorbitantly cheap to participate in. It may even be free in some cases if your employer elects to cover all administrative costs and fees. Moreover, there are no underlying fund fees since company stock is the only investment. Cost shouldn’t be an issue with either plan.

Contribution Limits

ESPPs come with a $25,000 hard dollar limit in any given year. Employer contributions to ESOPs are generally limited to 25% of covered payroll, and that limit includes contributions made to other plans such as a 401k.

Tying it all together

Both ESOPs and ESPPs are great tools to help you build wealth and prepare for retirement. You can participate in the growth of the company with someone else’s money (ESOP) or with your own money at a known discount (ESPP). And yes, your company may offer you both!

The primary considerations for purchase come down to portfolio diversification and taxes. Individual companies are subject to sometimes strange and idiosyncratic risks that broad markets rarely face. Over allocating to a single stock, be it purchases in an ESPP, your 401k, an ESOP, or any other variety other equity compensation plans can add a significant amount of risk to your retirement longevity. Concentrated single stock risk must be approached with caution.

Taxes are complicated, too, especially when offered in conjunction with other equity vehicles such as ISOs, RSUs, or NQSOs. These all have their own unique rules to how tax is applied, but the complexity shouldn’t dissuade you from contributing. Nobody has gone on to gain financial independence by sitting on the sidelines. Use these vehicles when and where you can and as part of a broader savings strategy.

When in doubt, talk to the experts.